CommoditiesSeries 3

Commodities Series 3 - Diversified Commodities Index Long Only

The Units in Sequoia Commodities Series 3 offer 100% leveraged exposure to the BNP Paribas Energy & Metals Enhanced Roll ER Index (”the Reference Asset or Index”) with a 15% Target Volatility mechanism over a 2 year period and the potential to receive an uncapped Performance Coupon at Maturity dependent on the Strategy Value Performance, adjusted for changes in the AUD/USD exchange rate during the Investment Term.

Sequoia Commodities - Series 3 Performance

| Date | Reference Asset Level | Indicative Unit Value* | Performance |

|---|---|---|---|

| 30-Jun-2021 | 100.00 | $1.10 | 0.00% |

| 30-Jul-2021 | 103.81 | $1.11 | 3.81% |

| 31-Aug-2021 | 103.09 | $1.11 | 3.09% |

| 30-Sep-2021 | 106.25 | $1.14 | 6.25% |

| 29-Oct-2021 | 109.90 | $1.145 | 9.90% |

| 30-Nov-2021 | 104.00 | $1.104 | 4.00% |

| 31-Dec-2021 | 107.58 | $1.117 | 7.58% |

| 31-Jan-2022 | 111.00 | $1.149 | 11.00% |

| 28-Feb-2022 | 117.40 | $1.237 | 17.40% |

| 31-Mar-2022 | 130.53 | $1.289 | 30.53% |

| 30-Apr-2022 | 130.32 | $1.308 | 30.32% |

| 31-May-2022 | 131.96 | $1.340 | 31.96% |

| 30-Jun-2022 | 125.60 | $1.277 | 25.60% |

| 29-Jul-2022 | 125.65 | $1.273 | 25.65% |

| 31-Aug-2022 | 125.24 | $1.274 | 25.24% |

| 30-Sep-2022 | 117.74 | $1.207 | 17.74% |

| 31-Oct-2022 | 119.73 | $1.21 | 19.73% |

| 30-Nov-2022 | 124.47 | $1.241 | 24.47% |

| 30-Dec-2022 | 120.07 | $1.197 | 22.27% |

| 31-Jan-2023 | 119.46 | $1.184 | 20.78% |

| 28-Feb-2023 | 114.475 | $1.146 | 16.16% |

| 31-Mar-2023 | 115.4411826 | $1.156 | 17.289% |

| 28-Apr-2023 | 113.942 | $1.142 | 15.850% |

| 31-May-2023 | 106.792 | $1.073 | 7.858% |

| 30-Jun-2023 | 108.10 | $1.085 | 9.176% |

* This represents an indicative level for unwinding your investment on the reporting date and is an indication of the market value of the investment.

** The Gross Performance refers to the performance of either the underlying Reference Asset or Strategy Value as at the end of the relevant month, whichever is applicable depending on the terms of the Termsheet PDS.

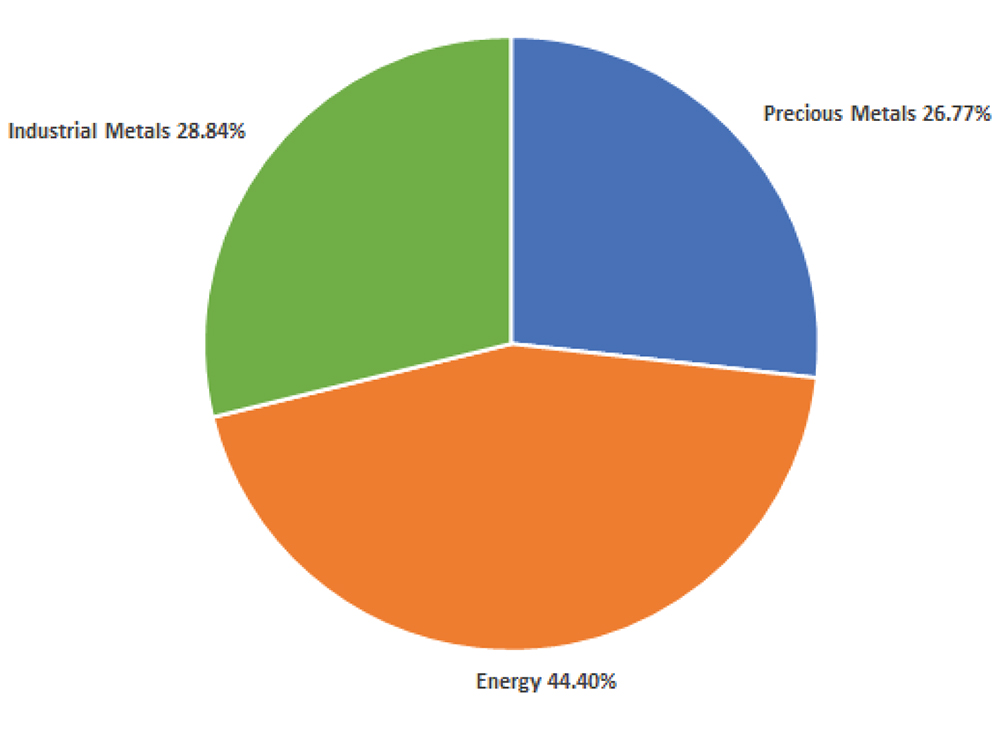

The Index offers a long only, diversified exposure to the commodity asset class, excluding Agriculture and Livestock. The key features of Index are outlined below:

- Diversification across 3 commodity sectors using the same sector diversification of the industry benchmark commodity index known as the as the Bloomberg ex- Agriculture and Livestock Capped Total Return Index (“The Industry Benchmark Index”):

1) Industrial Metals;

2) Precious Metals; and

3) Energy

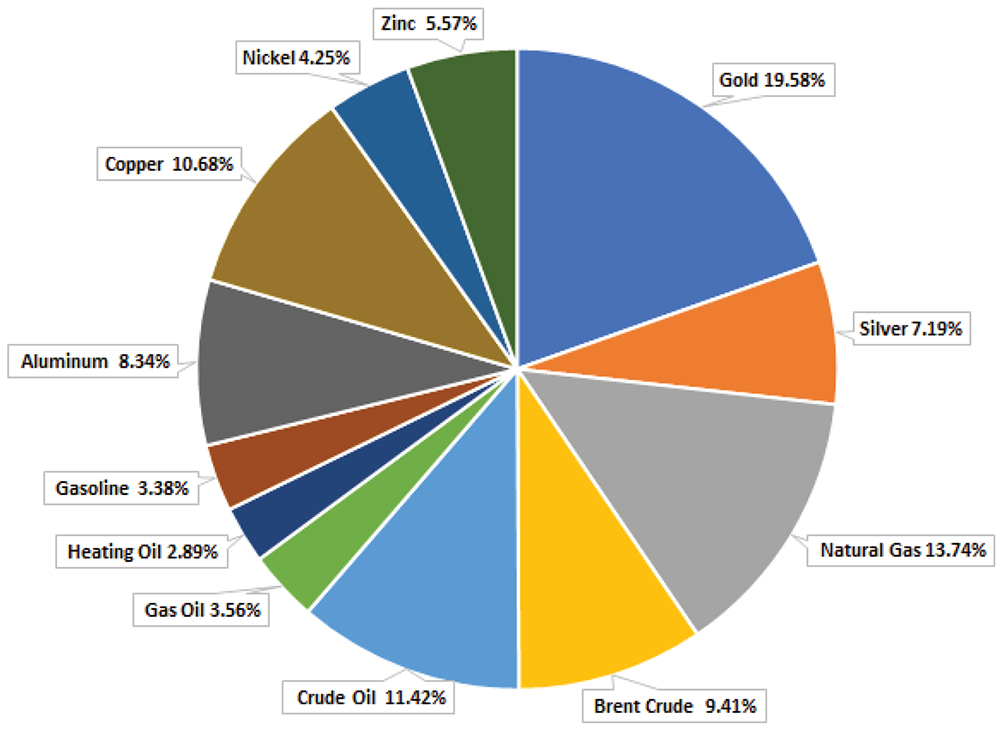

As at 15 April 2021, the sector allocation of the Index was:

- The individual commodity weights within the Index are calculated by reference to the following:

1) As a first step it uses the same weights as those included in the Industry Benchmark Index. The Industry Benchmark Index uses liquidity and production data to determine the weights of each commodity within that index;

2) As a second step, a daily weight capping mechanism is applied to ensure that the sum of the weights for all commodities included within the Energy sector does not exceed 35% and that no individual commodity within the Index exceeds 20% on a daily basis.

Find out more about Sequoia Specialist Investments

Complete the form below and we’ll be in touch as soon as possible.

Downloads

To find out more, and to download a copy of the Term sheet PDS and Master PDS, please click on the links below

Find out more about Sequoia Specialist Investments

Complete the form below and we’ll be in touch as soon as possible.

Reference Asset Starting Value

Find out more about Sequoia Specialist Investments

Complete the form below and we’ll be in touch as soon as possible.

Find out more about Sequoia Specialist Investments

Complete the form below and we’ll be in touch as soon as possible.